I was recently interviewed by Peter Mcarthy as part of his industry leadership interview series. With the financial year coming to a close once again, he wanted to talk about what business owners can be doing to prepare and make the process as easy as possible.

Peter McCarthy:

Good afternoon, and welcome….

Today we launch the first of a series of Industry Leadership interviews and webinars. Today, it’s a timely reminder to finalise preparations for the End of Financial Year for your business.

For everyone joining us, feel free to send us your comments or any questions you may have about preparing for EoFY and we will add these to the discussion, or we will leave time at the end of the session and answer as many as we can.

I would like to welcome my friend and colleague of many years, Ian Senior from Refresh accounting. Welcome Ian.,…

Ian Senior:

Hi Peter and hello everyone, I really appreciate this opportunity to join this discussion and to share some end of financial year preparation tips today with everyone.

Peter McCarthy:

Ian, to assist everyone joining us today, can you give us a brief introduction to your background and your business Refresh Accounting.

Ian Senior:

Yes, of course, I think that we all start our businesses with a dream or vision. You and the others listening, will have imagined yourself taking a long weekend off, camping, visiting friends, relaxing with cash in the bank and then as owners of your business you found yourself frustrated by the complexities of running it, frustrated that you spend too much of your valuable time running it, stressing about cash flow and struggling to find a private life. All we really wanted to do was do the thing that we’re good at. The issue though, is that you’ve never been trained to do the business stuff, and you feel like you’re learning on the fly. It’s hard work!

So, to put it simply, our aim is to help businesses improve and become more profitable so that business owners have cash to do the things that they love to do and the time in which to do them.

Personally, I’m a Chartered Accountant and have been doing this sort of work, either for an employer or for clients for over 30 years.

Peter McCarthy:

Ian, before we start talking all things financial, accounting and business strategies, should we commence with a “mild mannered” disclaimer about what we are suggesting today?

Ian Senior:

I think we’d better, otherwise we could find ourselves in trouble with the tax people and we don’t want anyone jumping in and doing something that isn’t suitable for them.

So, it’s important to note that firstly, I’m not a tax agent and secondly any advice is general in nature. I strongly recommend that you look at this discussion as a means of gathering information and then you follow up with your tax agent to get advice that is specific to you and your circumstances.

In fact, as a general rule, I always suggest that you talk to your tax accountant about your tax and Super before the year end, preferable as early as February when you are doing your BAS returns for December, so that you can really plan your tax affairs and not be in a mad rush, missing opportunities at the end of the tax year. That’s what the wealthy people do and they pay a lower percentage of tax than the vast majority of the rest of the population do.

Peter McCarthy:

Now, we know there are simple and essential tasks that businesses need to follow regarding tax compliance. Is there a resource that we can all use?

Ian Senior:

There are 3 good resources Peter.

Firstly, www.business.gov.au is a really useful website with a number of checklists to suit all sorts of business requirements;

Another is the ATO, again there is a host of information to be found at www.ato.gov.au

Finally, there is your own tax agent. While the ATO and the business.gov.au have lots of information, only your tax can give you accurate advice relating to your specific circumstances. And your tax agent is representing you, the other two resources are representing the government.

Peter McCarthy:

You mentioned earlier that you would give some general advice to us so that we can prepare for the End of Financial Year. What is that general advice?

Ian Senior:

To my mind there are 5 items of general advice that everyone should consider and then go and ask their tax agents as soon as possible, they are, spending money, buying equipment, client invoice, timing, stopping work and superannuation contributions. I’m sure that everyone has heard most of these before, but it doesn’t do any harm in going over them again.

So, spending money. Many businesses spend up in June to reduce their taxable profits, you buy everything under the sun to avoid paying tax. That’s OK, it’s a valid thing to do, unless you buy things that you can’t actually claim as a tax deduction. So make sure that what you want to buy will benefit you from a tax perspective. Also, now this bit I’ve been saying to clients ands businesses for over 30 years, don’t spend a dollar to save 30 cents! If you don’t need it, don’t buy it. Sure, if your work vehicle needs new tyres buying them at the end of June instead of the first of July will bring forward the tax deduction with no impact on the cash that you have to spend, but otherwise don’t spend just to reduce your tax. You’re usually better off spending the extra with your tax agent and getting better long-term strategic advice. Remember, I’m not a tax agent, so I’m not drumming up business for myself!

Now, buying equipment. Again this is a common tactic used to reduce taxes and with the new Instant Asset Write-off provisions that allow small businesses to write off capital items up to $150,000 in the year of purchase there will be many of our listeners already utilising this option. In addition to the don’t spend a dollar to save 30 cents mantra, there are a couple of points that I think mean you really need to have a discussion with your tax agent:

Firstly, equipment has to be in place before the end of June, so buying an item and paying for it in full may have no benefit to you if it isn’t delivered or installed by 30 June;

Secondly, it’s my understanding that the Instant Asset Write-off has the potential to create losses that can affect businesses set up using family trusts and with division 7A loans, franking credits etc. so again, talk to your tax agent, they will know your circumstances and give you the best advice.

Perhaps the most incorrectly used tactic is delaying issuing invoices to clients to July to defer the income. It can work if the actual work isn’t happening until July, but if the work is done in June then it’s illegal to delay the invoice until July. So, you need to be really careful with this and the broad rule is don’t do it. As an aside, I would also say that delaying invoicing means delaying the cash going into your account.

Now, stop working. I find this one the most bizarre, but as I’ve come across it a few times I’m mentioning it. I can still remember the first time I came across this. I was a partner in a firm of accountants in London and a client was sitting opposite me proudly telling me that he hadn’t work for two months because he didn’t want to pay higher rate tax. I can’t remember how much he was earning but let’s say that it was about 10,000 per month. So, I politely pointed out that by not working for two months, sure he’d potentially avoided paying something like 8,000 pounds in tax, but that meant he’d avoided earning 20,000 pounds and he was therefore 12,000 pounds worse off.

The look on his face clearly indicated that he hadn’t looked at it from that perspective, he just didn’t want to pay higher rate tax. The mantra here is sort of opposite the spending money one, don’t not earn a dollar to save 30 or 40 cents in tax.

Finally, superannuation. Currently the maximum pre tax contributions you can make, which include Superannuation Guarantee Contributions, if you’re an employee, is $25,000. In addition, you can make post tax contributions up to $100,000 per year and if you haven’t done that before you can add in two more years worth, so if you have the cash you could contribute up to $300,000 after tax contributions before 30 June. One of the main things to remember with Superannuation is that the contribution limit is based on the actual cash going into the fund in the tax year, not what was due to go in. The example here is, if you’re an employee and your Superannuation is paid by your employer after the end of each quarter, then your current year contributions will already have been paid because it would be the Super for the June 2020 quarter, paid in July 2020, the September quarter, paid October, December quarter paid in January and the March quarter paid in April. If you haven’t yet paid up to the maximum of $25,000 then you could look at topping this up before the end of June.

As has been said, you need to go and see your tax agent and clarify what you should and should not do.

Peter McCarthy:

Great, thank you Ian…….From a strategic standpoint, now is both a reflective time (to look at the current year), but also a planning time to look into the year ahead.

What are some of the recent changes SME business need to be aware of?

Ian Senior:

There are a few things that have changed, for example:

The Instant Asset Write Off for assets costing less than $150,000 has been extended to 30 June 2023;

The Superannuation contributions are increasing to $27,500 per year from $25,000 for pre-tax contributions, including Superannuation Guarantee Contributions; and

The post-tax Superannuation contributions is increasing to $110,000 per year from $100,000.

Other planning matters that should be considered include federal and state government grants. I’m not going to go into the State ones, as there are a lot that may be available, and they are different depending on the State that you are in. There are quite a few federal grants too and it’s well worth looking at joining a grant watch or notification system such as Grant Connect to keep yourself up to date with potential grants.

The one grant that I will mention though is the federal ‘Boosting Apprenticeship Commencements’ grant. This one is well worth checking out to see if you can get both existing and new employees covered as it can be worth up to $28,000 per employee over the next 12 months. The grant details can be found at www.dese.gov.au/boosting-apprenticeship-commencements. Don’t be scared off by the word ‘apprenticeship’ as it includes trainees undertaking certificate II or higher.

Peter McCarthy:

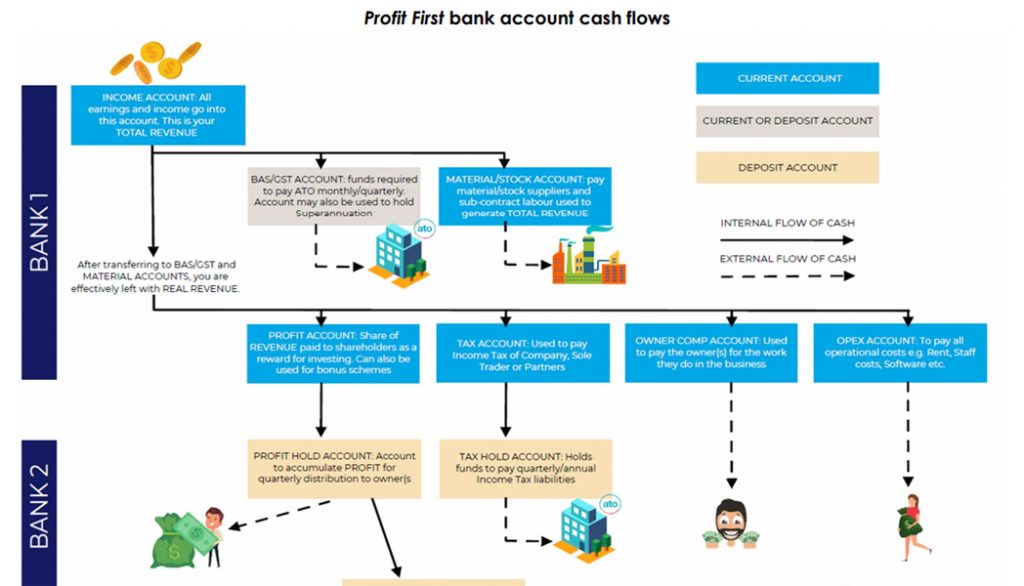

You have helped PestIT with new strategies to improve cash flow, which is critical to both inventory and service-based businesses. I know that you refer to this as the ‘Profit First’ cash flow strategy, some others may know it as bucket accounting – can you expand on this technique and how that works?

Ian Senior:

I know that we don’t have a lot of time to go into real detail on this, so I’ll try and be brief.

Profit First is a method of managing your cash by allocating all the income that you receive into different buckets, in actual fact different bank accounts, set up to meet the specific costs of your business. The aim is to ensure that you run your business so that it is always profitable and by that I mean that your business gives you a financial reward for investing in it, in the same way that you get a reward, through dividends, when you invest in shares on the stock market. Additionally, you will have funds to pay the tax authorities and yourself to reward you for the work that you perform on behalf of your business.

We all want our businesses to be successful and this really is a great cash management technique to achieve permanent profitability in our businesses.

Peter McCarthy:

I think this is an important way for businesses to focus on and isolate profit to ensure business viability. Can I invite you to do an Industry leadership interview just on this technique later in the year?

Ian Senior:

I’d be delighted to go into more detail at another interview Peter. In the meantime, you can find more information on my website www.refreshaccounting.com.au. There are some useful tools on there to help you with your businesses and more information on Profit First including a free download of the first two chapters of the Profit First book written by Mike Michalowicz. You can also email at [email protected] or call on 1300 895 200.

Peter McCarthy:

Ian, I know for PestIT your business planning, cash flow strategies and CEO services have been extremely valuable. These same strategies will be useful for any small business owner here…….so, how do business owners get in contact with you?